In its most recent report into coal (prices, supply and demand), the International Energy Agency presents plenty of data to depress a greenie. Or a certain teenage Swede.

In short, prices are up, demand is up and supply is reorganising as China and Russia disrupt supply chains.

First, look at prices.

Prices for thermal coal have doubled in less than a year. Note the fall off in prices in China since March 2022; that is likely to be entirely driven by the Ukraine war, sanctions on Russia and China buying excess Russian supply at discounted prices. In other words, it’s likely a temporary aberration.

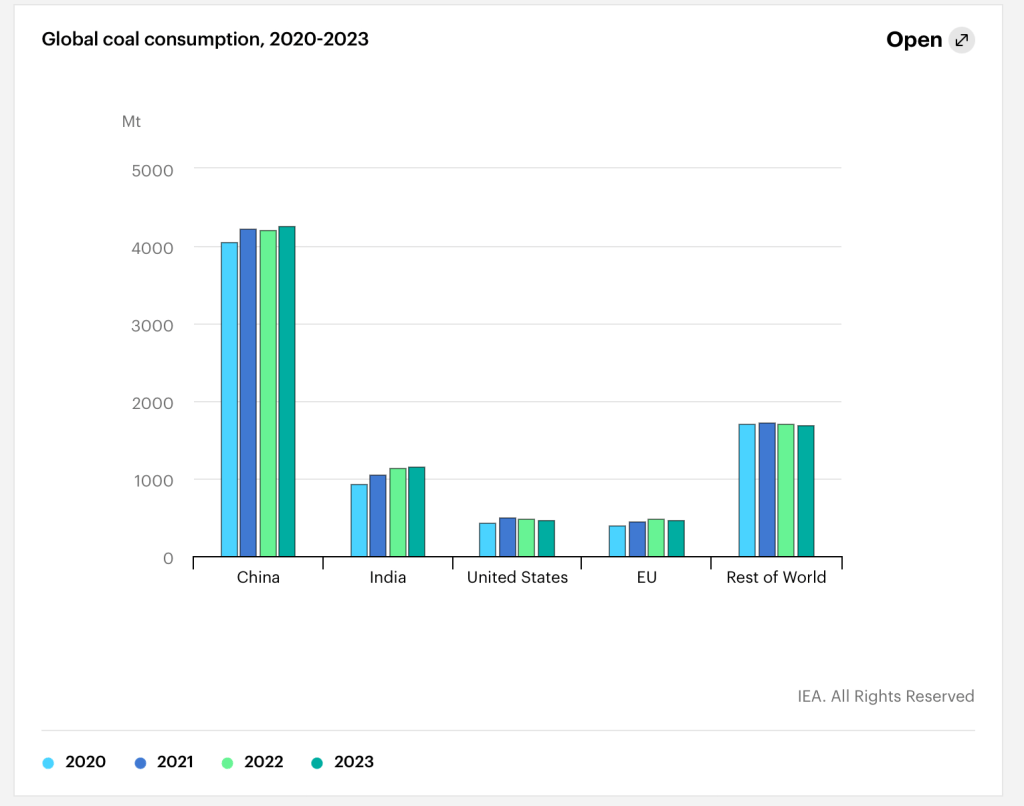

Next, look at global consumption.

2023 numbers are forecasts. On going increases in consumption, particularly in the two biggest markets, China and India. Finally, look at changes in supply lines.

Thermal coal is used for electricity generation, metallurgical coal is used for steel production. Indonesia has an impressive ability to increase supply, taking advantage of reductions in Australia, South Africa and Russia.

Supply lines have been pushed into reorganisation by various events and will probably remain stable once that process has worked through. After all, Russia is unlikely to want to increase exports to Europe after the Ukraine war is over, given the damage done to diplomatic relations, not to mention public attitudes, by economic sanctions imposed. Russia and China, perhaps with Iran, will be a more united trading bloc. Australia should be able to recover since it’s coal is well recognised as very high quality. We need to ensure that we don’t impose any self inflicted wounds on trade relations in the way the EU has.

Demand continues to grow. A global recession would put a dent in that growth, but given the circumstances of India and China, there appears no end in sight to on going high demand for coal. A recession would likely hit metallurgical coal demand more so than that of thermal coal.