I am not optimistic that we have seen the worst of inflation in Australia and I explain why in this post.

In recent days, the December 2022 quarter national statistics covering the money supply, producers’ prices and consumer prices have all been released. The data is worth reviewing for clues about what is yet to come.

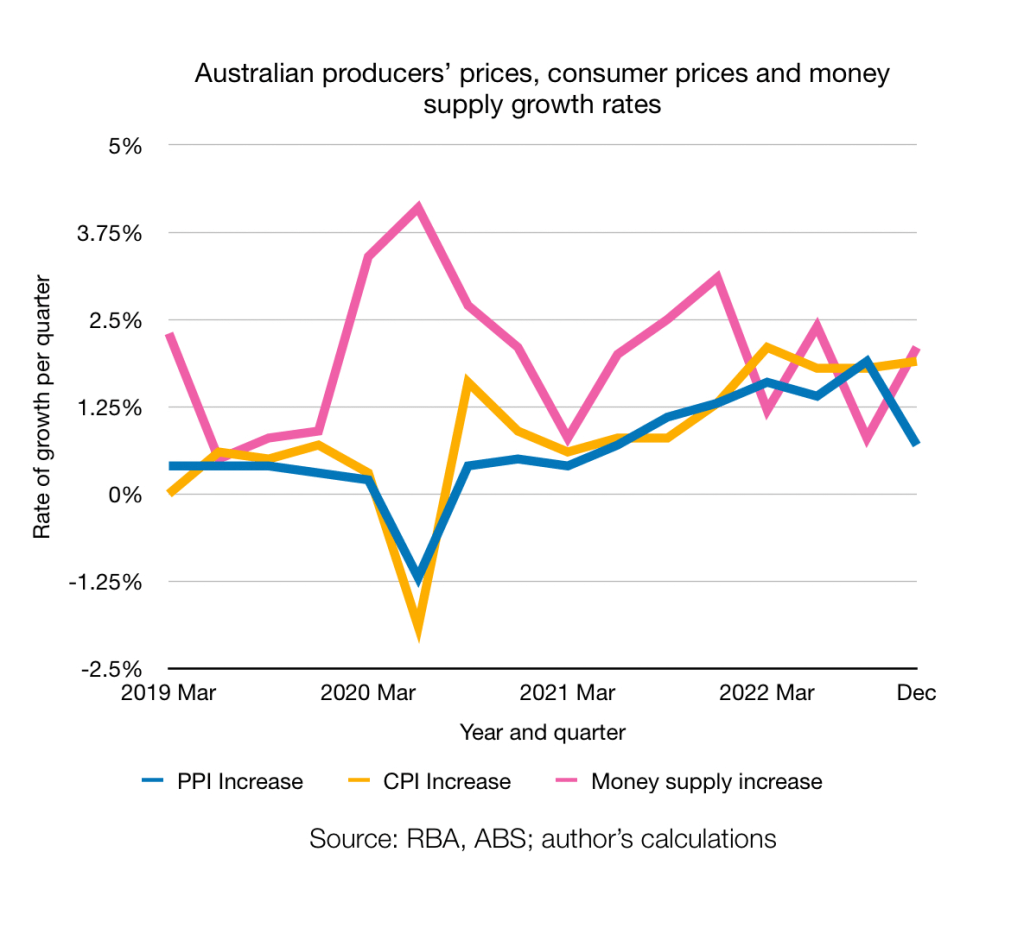

From this recent data, I have prepared this chart of growth rates in each of the money supply (Ms), producers’ prices (PP) and consumer prices (CP). The data is quarterly and covers the 4 years to December 2022 quarter. Ms is the Reserve Bank of Australia’s “broad money” definition. PP and CP are the Bureau of Statistics price indices for producers’ and consumers prices respectively.

I contend that inflation, as experienced in the economy as widespread increase in CP, always has at its root an artificial increase in the money supply. The sequence is an increase in Ms leads to an increase in PP leads to an increase in CP. As an adjunct, certain types of increase in Ms will also lead to a recession. I will explain those processes shortly, but first note the relative growth rates displayed in the above chart. The Ms growth continues. This suggests that the reduction in growth (not reduction, just slower increase) in PP in December 2022 could be temporary. CP continue to grow as long as PP are increasing.

Over the 4 years, the average annual growth rate in Ms was 8%pa.

The process by which an artificial increase in Ms leads to an increase in CP is as follows. The Ms increase generates easier financing options for entrepreneurs. Money is cheaper, loans are cheaper and entrepreneurs are now attracted to investment projects that previously were judged as unprofitable. They borrow money, invest in new plant, material, equipment, labour, patents etc aimed at satisfying future consumer needs on those longer term opportunities. This process results in higher demand among producers for producers’ goods, those raw materials that turn into machines and so on that can generate future consumption goods. Of itself, that bids up the prices of raw materials. It also bids up the prices of the producers’ goods that would otherwise continue to be used in current production processes. Over time, there is a rise in the cost of production and, to remain in business, producers must increase the prices of the final consumption goods.

What is not an artificial increase in Ms? If the Ms increase was due to a change in the consumers’ propensity to save, then the higher bidding for prices of producers’ goods for long term investment projects would be offset by a lower demand for the producers’ goods needed for short term consumption goods. That is, the consumers’ time preferences would have changed and they would be willing to forego some current consumption for greater consumption in the future. In that case, the production structure would change. It would take time, but it would not be an inherent cause of CP increases. However, if the rise in Ms was caused not by relatively more saving in the community but rather by an increase in bank credit, the inflationary process would be set in motion and sooner or later, the statistics bureau would be reporting CPI rises and every galah in every corner pet shop would be talking about the inflationary spiral.

Increases in Ms by bank credit is one of the primary means by which expansionary monetary policy is implemented by the central bank. The RBA can manipulate a number of levers to inject money into the economy out of thin air. This is what I refer to as an artificial increase. Such an increase in Ms is nearly always impossible for an entrepreneur to identify separately from a real increase in Ms owing to the community’s changed propensity to save. Heck, all the entrepreneur wants to know is the internal rate of return on a new project with the banks’ new loans. So they get the wrong message. They think the community wants to shift consumption away from some current goods to certain future goods. But what if the community hasn’t made that decision? Eventually, the investment project will not meet it’s cash flow modelled assumptions, the entrepreneur may well go bankrupt, resources are tied up in the wrong production structure and the mess needs to be sorted out – decommissioned, unwound, retrenched, etc. A recession is a necessary cleansing process, someone or other once said. True enough, but the pain of that cleanse is made much worse and for much longer the more the central bank tries to sustain economic activity through injecting more funny money into the economy. Did I mention that I believe central banks are unnecessary and in fact do much more harm than good?

Belatedly, the geniuses at the RBA have decided that we are at risk of inflation. (Who knew? Pretty much everyone awake, other than RBA executives and Modern Monetary Theory adherents.) So what has been their response? Manipulate the money supply levers to force interest rates up, thereby reducing growth in Ms, maybe even contracting Ms. In a way, that may suggest the RBA acknowledges the underlying truth of what I have explained here. But that may give those RBA chaps and chappesses too much credit. I don’t think they understand and instead jerk their knees one way or the other until something works. But if they are trying to contract Ms, the chart above shows that they aren’t succeeding. More adjustments needed, I suspect. More pain. More inflation and probably stagnant or diminishing economic growth.