I accidentally stumbled onto the website of the Reserve Bank of Australia (RBA) on a recent search for inflation data. Trust me, it was an accident. While I sometimes visit the RBA site for a laugh, I never go there to learn anything.

In this case, the RBA page gave an explanation of the causes of inflation. Stop me if you’ve heard this before: demand-pull, cost-push and inflationary expectations. Yawn. Decades after the twitterings of Keynes and Samuelson, the modern day RBA types still believe that rubbish.

Let’s work backwards from inflationary expectations. The RBA states that if people expect inflation, they will act accordingly and bid up prices and wages in anticipation of the loss of purchasing power. Raise your hand if you have ever successfully won a pay rise by telling your boss that you have expectations of inflation? You are likely to be no more successful than Oliver Twist was when asking for more thin gruel. Or have you ever convinced a client to pay a higher fee because of your inflationary expectations? While it is true that people may expect inflation, in no way does that mean that they can cause inflation.

Then consider cost-push inflation. The theory here is that the cost of doing business increases which must force up prices. The input cost increase may have come from higher wages (editor’s note: all those inflationary expectations at work?) or, a commonly cited example, an oil price shock. As a vital commodity, if the price of oil increases, that works its way through vast swathes of the economy, driving up the cost of production and hence driving up consumer prices.

If you switched off your critical thought faculties at this point, you may well be persuaded by that argument. So don’t switch off. Instead, think through the next step: if there is a generalised rise in prices caused by an oil price shock, how will the consumer finance that extra expenditure? If the total of my disposable income is $Y, how can I increase that to $Y+d? I may be temporarily able to by reducing savings, using credit but then what? The only way is to adjust my demand. I will be forced to buy fewer goods and services whose prices are rising and substitute in some others whose prices are not rising or are falling.

This necessary consumer reaction, across the whole economy, will result in an adjusted pattern of production based on the consumers’ adjusted pattern of consumption. Overall, prices will have changed, some demand will have fallen, some demand will have risen but the previous structure of consumption cannot be sustained. There can be no general increase in prices because they cannot be financed.

Unless, of course, the RBA steps in and manipulates the money supply. If the money supply increases, then general higher nominal prices can be financed because the consumer would have higher nominal wages. Real prices, real wages will not change but nominal prices and wages will be higher. This could be called demand-pull inflation. Demand-pull inflation cannot exist unless financed by an increase in the money supply.

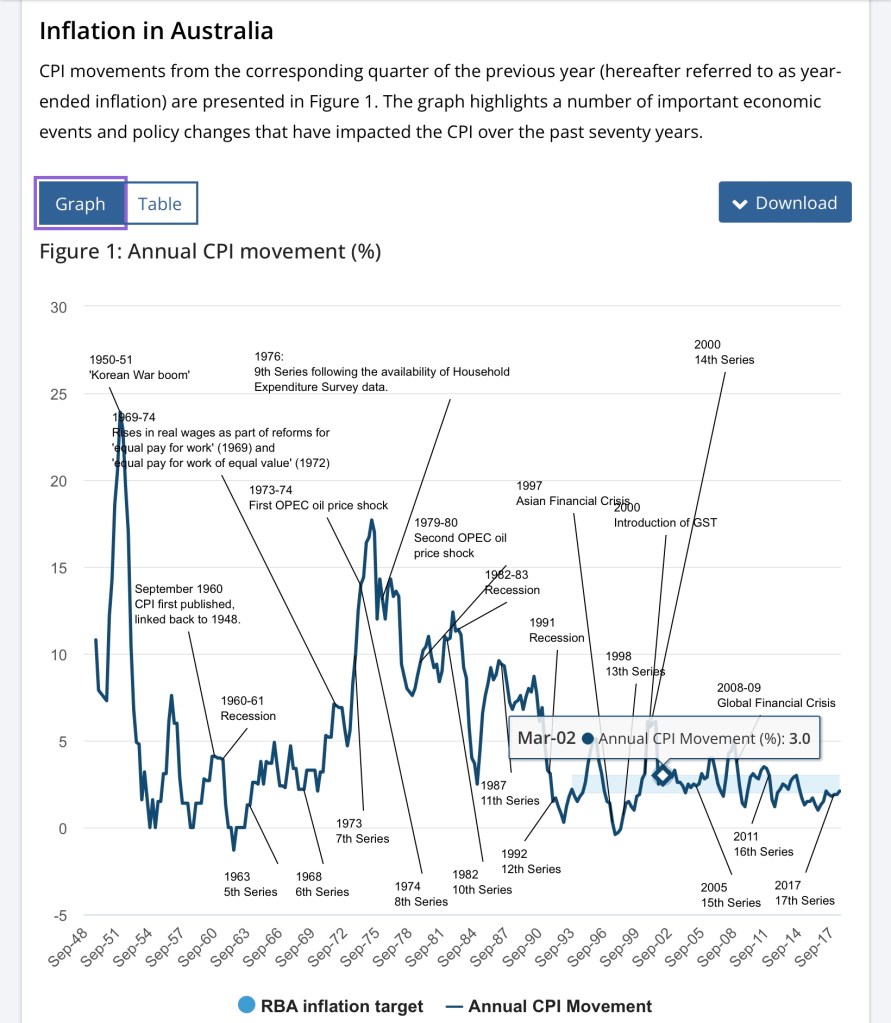

Here is a chart of Australian price inflation from the Australian Bureau of Statistics.

Look at the spikes with the Korean war and the OPEC oil price shock.

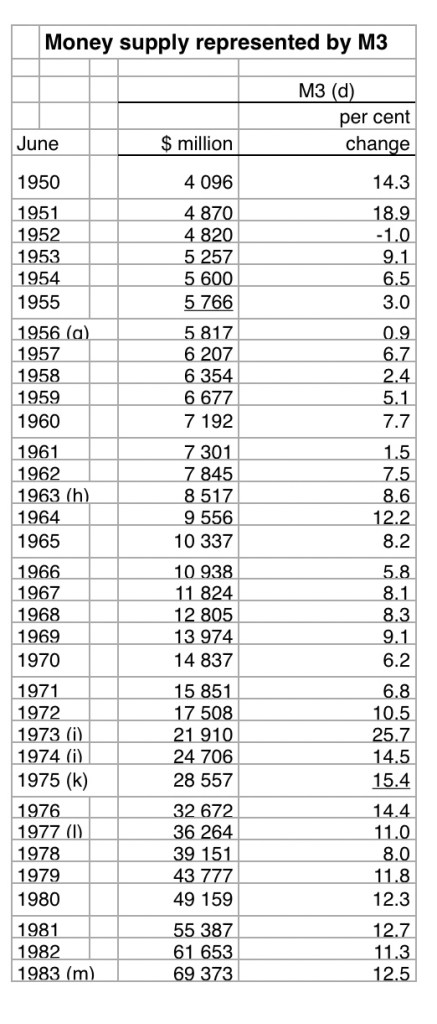

Now look at this table of growth in Australia’s money supply from the RBA.

Look at the spikes in the money supply growth rates at the time of the Korean war and the OPEC oil price shocks.

Nowhere in any of the writings of the RBA could I find reference to the growth in the money supply as having a role to play in inflation. Why not, I wonder.