The French are credited with saying that the more things change, the more they stay the same. The phrase is less elegant when expressed in English. Perhaps the most frequently quoted line of Guiseppe di Lampedusa’s novel ‘The Leopard’ is the Prince’s acceptance that ‘If we want things to stay as they are, things will have to change.’ George Orwell wrote, in his essay ‘The Lion and the Unicorn’, of England having ‘the power to change out of recognition and yet remain the same.’ Friedrich Hayek wrote of ‘the fatal conceit’ of those people who believe that central control and planning of a country’s economic output is possible, and even desirable. These are only a handful of examples of a history of observation and understanding of the challenges in achieving meaningful change in a society. Change is endless, although superficial unless the emotions of the people change. Continue reading

Economics

Fair trade coffee, quality certification and responsible investing

At the centre of each of these topics lies social activism that always progresses to economic rent-seeking. They start when certain people have a view that a market is failing in some way. Those people make their own judgement and decide that they want to change the particular market. They want to impose their views on the market participants. For example, in fair trade coffee, the central aim is to improve the working conditions and reward to local farmers and labourers in coffee growing areas. In quality certification, the certifying authority believes it is better able to judge quality than the consumer and so its stamp of approval adds an element of protection to the buyer. With responsible investing, the picture is a little confusing at present. Responsible investment agents are not clear on their value proposition – on one hand they present their case as ensuring (their) ethics are brought into the investment decision and so certain investments will be automatically excluded. On the other hand, they try to present this approach as good for investment returns. Well, it can’t be both. More on that later. Continue reading

Gathering voices

Some months ago, I posted a piece here saying that the problem with the economy had nothing to do with high interest rates. Cutting interest rates further would not work. Since then, the Reserve Bank of Australia has cut the official cash rate from 2.5%pa to 2.0%pa.

If only a few more economists would make their views known, such as here, and a few more would stand up to the uninformed mainstream economics doctrines* taught mostly everywhere since the death of Keynes, then we would begin to see an improvement in public policy. Let’s hope.

* To help kickstart thinking, how many borrowers pay 2%pa on their borrowings? What is your mortgage rate? What is your credit card rate? What is the cost of capital under a debt finance model for a small business? There are thousands of interest rates in the market, not just one with stepped margins. Why would that be? What does that mean for the IS/LM model and ‘the’ interest rate?

General Election in the UK

The election result in the May general election has seen the Conservative party win majority Government. This is undeniably the best result for the UK and interested on lookers. To commentators, the result is a huge surprise. Pre poll accepted wisdom was that there would be no single party majority but instead a messy cobbled together and inherently unstable coalition, possibly with Labour as senior partner. Fortunately, that was avoided.

The UKIP party won approximately 13% of votes, yet only 1 seat, due to the workings of the electoral system. In contrast, the Scottish National Party won 5% of the vote and 56 seats. Go figure.

What Mr Cameron should now do is recognise that the Conservative majority, plus the 13% vote to UKIP, shows that the UK population appreciates economic management. To date, the Government has made modest progress in correcting the economic mismanagement of Labour. Key action is now needed to reduce the budget deficit, reduce statism, reduce welfare abuse and reward individual responsibility. Profit is not a dirty word – profits, and reward for effort, must be admired, not demonised. Tax rates should be reduced, trade liberalised and regulations scrapped. Mindless regulation imposed by the EU must be resisted or ignored – yes, Brexit would be an excellent outcome.

Mr Cameron is not in the mould of Mrs Thatcher or Mr Reagan. But he should take heart that displaying the attitude of those two great leaders to economics will gain him electoral respect, despite what the leftist media says. Please get on with it.

Does this represent effective retirement incomes policy?

The Australian Retirement Incomes system is based on the three pillars of a taxpayer-funded age pension, compulsory occupational superannuation and then everything else including voluntary savings, causal work, family support etc. The introduction of compulsory occupational superannuation in 1992 has not done much to relieve pressure on the first pillar.

This chart shows how a retirement income is generated in one particular case. The hypothetical individual in this chart enters full-time work at age 21 on a salary of $45,000pa. What follows are 44 years of continuous work, with the salary rising at a real rate of 1.5%pa, superannuation contributions are at 12% of salary over the whole term and the investment return is 3%pa real before fees and taxes. On retirement at age 65, our hypothetical worker targets a retirement income of 50% of pre-retirement income.

It is not inspiring. This person would be unusual among Australians to have a full-time career with no employment breaks, through choice, necessity, unemployment, parenting etc. The earned income is better than the median. The rate of contribution is 12% of salary throughout – at present, most people have no more than 9.5% saved. The real investment return of 3%pa will require everything to go well over a very long period, including through retirement.

The conclusion is that the taxpayer is funding about half this person’s retirement income, until about age 90, when the taxpayer takes over 100% funding obligations.

The smell of tax change is in the air

Can you smell it? The prevailing winds at this time of year come from the direction of Canberra as the Government and public servants in the departments of Treasury and Tax work out the policy changes that will form part of the Budget night speech by the Treasurer in early May. When I turn my nose towards Canberra, I can definitely detect the smell of tax changes.

The federal Government executive works feverishly ahead of the Budget in formulating ideas for policy change. Sometimes, the ideas are good, sometimes they are not so good and sometimes they are positively barmy. The work rate is high and the stuffiness in the office air in Canberra gets worse as each day moves into night and the deodorants applied that morning have long ago given up the good fight. At this point, the officials can open the windows or turn up the air conditioners. Usually, it is in the office where the policy idea might be considered by Sir Humphrey as ‘courageous’ that the window is opened. This lets the smell of the idea waft out into voterland and the reaction of voters is a guide to Government as to the acceptability of the idea. In other offices, the windows remain tightly shut and no whiff of the idea gets out until shortly after 7:30pm on the night of the Treasurer’s Budget speech.

Right now, the tax changes under serious consideration, judging by the air wafting from Canberra, include changes to franked dividends, age pension eligibility and negative gearing. Continue reading

Allowing access to superannuation assets to purchase first home

Another kite being flown? The Federal Treasurer, Joe Hockey, suggested that the law could be changed to allow first-home buyers access to their ordinarily preserved superannuation savings. Supposedly, this would help them finance the price. The cost of housing in Australia is very high and getting into the market is hard.

If that is a kite, it should be shot down. Such a change in policy would be a very bad decision. The high price of housing is not caused by young people not having access to super money. Nor would the price pressure be eased by allowing such access. In fact, the price pressure would be made worse as extra demand chases an unchanged supply. The prices would rise, the first home buyers would have depleted their super savings and the transfer of assets would have gone to sellers of housing.

Thanks to Art Laffer

Dr Art Laffer is in Australia this week. I enjoyed listening to him deliver a speech to IPA members and guests in Melbourne on Wednesday. When I say ‘deliver a speech’ I mean entertain a large group of people with wit, humour, optimism and humility in a lively discussion full of historical significance and anecdote. He explained his a priori theories and backed them up with evidence. For those of you who have enjoyed the short film of Art having a commemorative lunch with Dick Cheney and Don Rumsfeld, he is just as engaging with an audience of strangers as he is when lunching with his friends of 40 years or more.

Dr Laffer is undoubtedly one of the most influential people of the last 40 years.

Economists, groupthink and dark clouds

The official cash interest rate in Australia is 2.5%pa. According to business press surveys of “leading economists”, most believe that the Reserve Bank of Australia should cut the official rate very shortly. Weak economic growth and rising unemployment worry the economists and their policy response recommendation is to reduce interest rates. We shall find out soon enough if the RBA takes that approach, but if the business press is correct, what is it about these economists that makes them unable to see that if interest rates are already at low levels and economic growth is insipid, then the problem is not likely to be a high interest rate. Can’t they see what happens in other countries where official interest rates have approached zero and it has not spurred economic activity?

So-called leading economists who argue that more artificial credit expansion, in an environment that has already suffered more artificial credit than is reasonable, are firstly demonstrating that they have no clue as to what has caused the mess nor how to get out of it. Secondly, they cling to each other and reinforce their collective group-think views because they have little else to comfort themselves that they know what is going on. This fear on their part and their response to argue for more policy medicine along the same lines that is making the patient sick is leading to ever increasing dark storm clouds looming on the economic horizon.

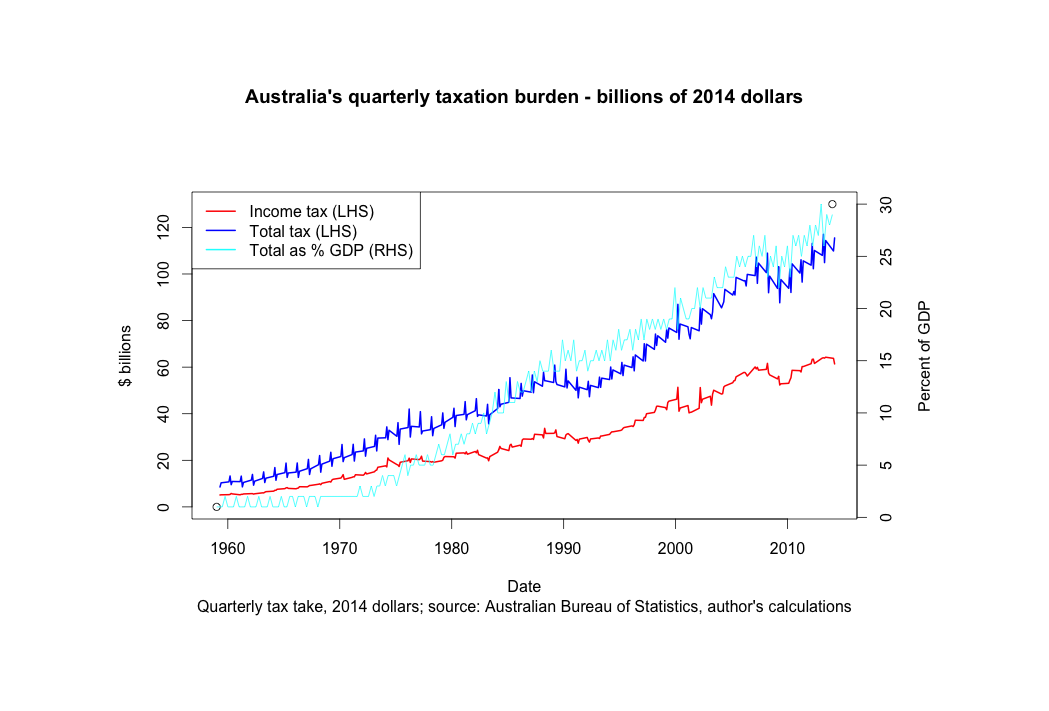

Australia’s increasing tax burden

The tax burden in Australia has been on the rise for decades. In particular, the total tax take, expressed as a percentage of GDP, has accelerated from the early 1970s. The chart below has all dollars expressed in the equivalent 2014 values. The total tax burden has risen from around $10bn per quarter in 1960 to $27bn per quarter in mid 2014. Of this, income taxes have been rising, but not at the same rate as total taxes. The total tax burden as a percentage of GDP has risen over this period from 1% to 30%.

This trend is unsustainable. No economy can survive an ever increasing tax burden. Some other countries have already passed a tipping point. Australian political leaders need to take note.