If you care to look at the financial press, personal investment magazines or the information brochures published by superannuation funds, you could be excused for concluding that a new incurable disease has become entrenched in the community – longevity. The fear of living too long and running out of money in retirement is affecting more and more people, particularly in the light of weakening Government finances which are needed to pay for the age pension.

Enormous volumes of papers and investment brochures, armies of financial advisors, whizz-bang calculators and projectors available on-line are all at work on the population. The message is almost always that Australians need to save more for retirement. People are constantly reminded of how long they are expected to live and how much money they will need to meet living expenses. However, funding a comfortable lifestyle in retirement is increasingly looking beyond the capability of the average person.

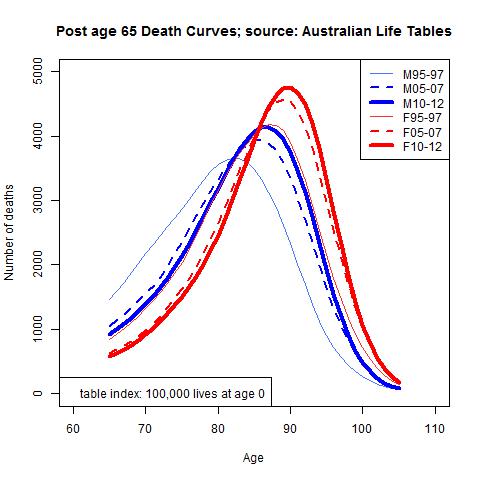

The expectation of life of a 65 year old male in Australia is now just over 19 years and fractionally over 22 years for a 65 year old female, according to the Australian Life Tables 2010-12 recently released by the Australian Government Actuary. At the start of the 20th century, when the Government funded old-age pension was introduced in Australia, the expectation of life at age 65 was 11.3 years for males and 14.2 years for females. If life expectancies continue to improve, then at some point, it becomes impossible for the average household to fund retirement. The value of wages earned on a life-time of labour over a 45 year time-frame, say from age 20 to age 65, is simply not enough. If the retirement age is held constant at 65, the problem has no solution – it does not matter how much people are cajoled about saving more, the preference for food, clothing, shelter, medicine in the present will always be stronger than the preference for a greater superannuation balance that could be needed many years into the future. Continue reading